Mining Rig Prices Increase by 24% as Trump's Tariff Policy Hits US Bitcoin Mining Industry

Original Article Title: How Trump's Tariffs Will Affect Bitcoin Mining

Original Article Author: Jaran Mellerud

Original Article Translation: Deep Tide TechFlow

Trump's tariff policy will have a significant impact on the Bitcoin mining industry. Here is an analysis of the policy's impact on the industry.

On April 2nd, Trump announced comprehensive new tariffs on imported goods aimed at strengthening U.S. trade balance. The Southeast Asia region was hit the hardest, impacting the Bitcoin mining machine supply chain profoundly. This region is home to most of the major mining hardware manufacturers, including Bitmain, MicroBT, and Canaan.

Furthermore, as the U.S. holds 36% of the global hashrate, these tariffs could significantly affect miners' profitability, hardware prices in the U.S. and abroad, and the global hashrate distribution.

Before delving into the multifaceted impact of these tariffs on the Bitcoin mining industry, let's first briefly explain how tariffs work.

How Do Tariffs Work?

Tariffs are taxes imposed by the government on imported goods, usually aimed at protecting domestic industries by raising the prices of foreign products. When tariffs are in place, importers must pay a certain percentage of the declared value of the goods to customs upon entry.

For example, if a U.S. company imports $1,000 worth of electronics from China and the tariff rate is 54%, the importer must pay an additional $540 in tariffs, bringing the total import cost to $1,540. This increased cost is often passed on to consumers or reduces the importer's profit margins.

Tariff History: The U.S.-China Trade War and Its Ripple Effects

Bitcoin mining is a global industry, with the U.S. being a significant player, and the trade war and resulting tariffs have already impacted the industry. However, in the past, companies in the industry have found ways to circumvent these tariffs. In the following section, we will explore how tariffs have historically affected the Bitcoin mining supply chain and what strategies companies have employed to bypass these tariffs.

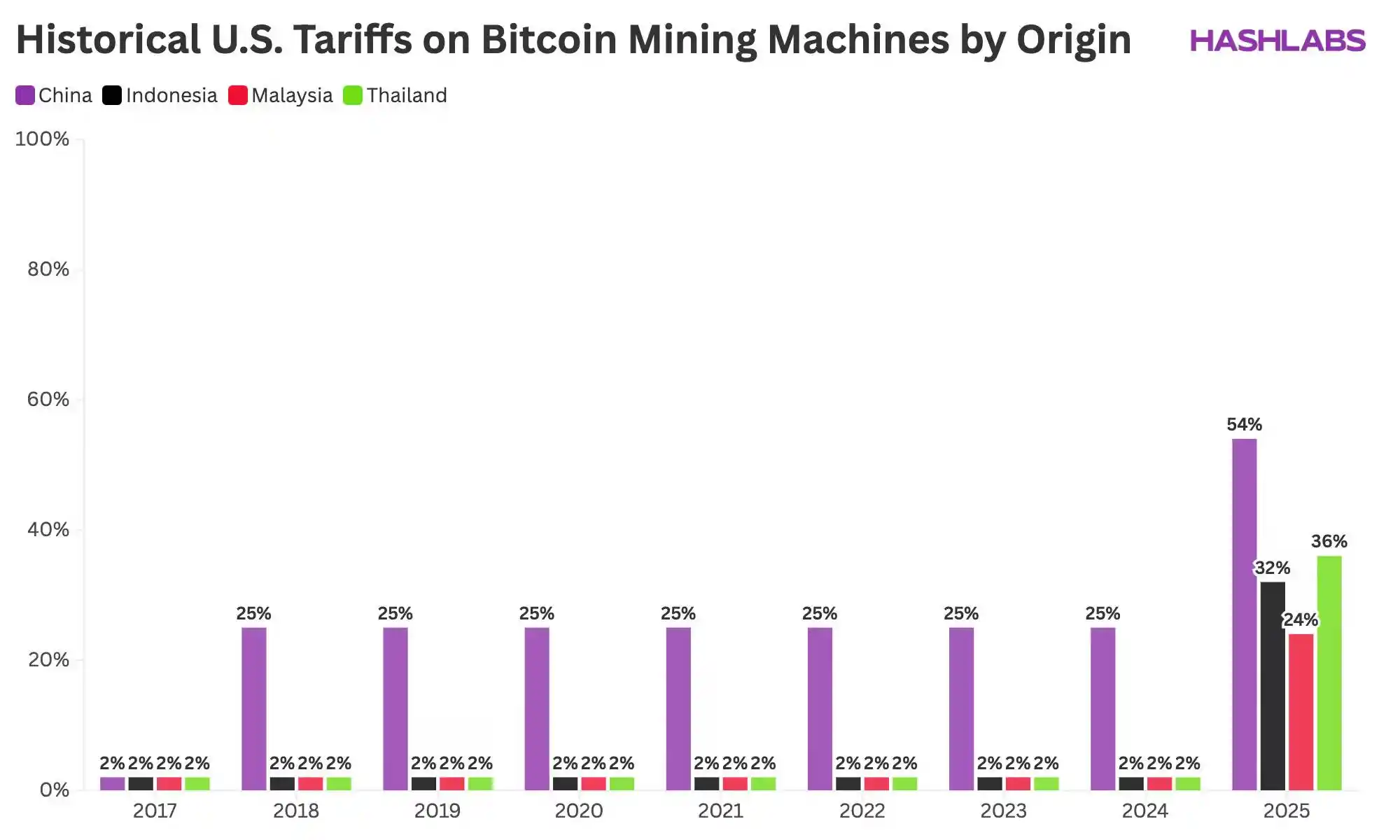

In 2018, the U.S. government imposed a 25% tariff on a range of Chinese goods, including electronics, as part of the U.S.-China trade war.

In response, companies such as Bitmain began seeking ways to circumvent these high tariffs. They shifted their production from mainland China to Southeast Asian countries such as Indonesia, Thailand, and Malaysia, where exported goods to the US are either tariff-free or subject to lower tariffs—typically ranging from 1% to 3% for electronic products.

This strategy was effective until earlier this month when Trump raised tariffs on imports from Indonesia, Malaysia, and Thailand to 32%, 24%, and 36%, respectively. As a result, companies like Bitmain and MicroBT can no longer entirely avoid these high tariffs, which were initially targeted at goods imported from China.

In the following sections, we will elaborate on how these newly imposed tariffs will impact the Bitcoin mining industry.

Significant Price Increase Expected for Mining Machines in the US

The most direct and noticeable impact of the tariffs is that mining machine prices in the US are expected to increase significantly.

As Ethan Vera pointed out in "The Mining Pod" show: "...any company operating in the United States looking to purchase mining machines will need to pay an additional 22% to 36% for these machines." This aligns with our data.

However, the 22% price hike only applies to imported mining machines. Currently, there is still a substantial amount of mining machine inventory in the US. Based on Bitmars' pricing data, there is a 13% to 25% price difference between mining machines in the US and those in Hong Kong. As the US inventory diminishes, this price difference could narrow to 22%, plus a small shipping cost.

The graph above shows the final cost of importing a $1000 Bitcoin mining device into the US and Finland before and after the introduction of equivalent tariffs. Finland, like most other countries, has no tariffs on electronics imported from Asia—we use it as an example because we mine there.

As shown in the graph, due to approximately 2% tariff, the initial cost of importing a mining machine to the US was slightly higher. However, after the introduction of the new tariffs, the lowest cost of a $1000 mining machine in the US increased to $1240. This is a significant increase. Meanwhile, in Finland and most other countries, the cost of a $1000 mining machine remains the same due to the absence of tariffs.

In an industry as cost-sensitive as Bitcoin mining, a 22% increase in mining machine prices may render operations financially unsustainable. In the subsequent sections of this article, we will explore how these changes affect mining profitability in the US compared to other regions.

Mining Machines Outside the US May Become Cheaper

As mining machine prices within the US rise, prices of mining machines in other parts of the world may see an opposite downward trend.

The demand for mining machines shipped to the US is expected to plummet, possibly approaching zero. Given the US has been a dominant player in the ASIC (Application-Specific Integrated Circuit) market, representing nearly 40% of the global hashrate, the sharp decline in US purchases will lead to a significant drop in global demand.

With reduced demand from US miners, manufacturers will face an oversupply of inventory originally intended for the US market. To clear this surplus stock, they may need to lower prices to attract buyers from other regions.

While it's difficult to precisely predict how much mining machine prices will drop—since mining profitability also impacts prices—we can draw a conclusion based on fundamental economic principles: a decrease in demand for an asset usually leads to a price drop.

This price drop will make it easier for miners outside the US to expand further, which may also result in the decline of the US's share in global hashrate that we will discuss next.

US Share in the Global Bitcoin Mining Industry Will Decline

Since China banned Bitcoin mining in 2021, the US has been a dominant force in Bitcoin mining. According to data from Hashrate Index, the US currently holds 36% of the global hashrate.

Like any business activity, the core of Bitcoin mining lies in balancing risk and reward. Over the past four years, the US has attracted significant mining investment as it is seen as one of the lowest-risk environments in the world, with political stability, abundant energy, and a liberalized electricity market. Additionally, miners have so far avoided major import tariffs, helping them control capital expenditures. These factors together have created an unparalleled risk-reward balance.

To understand how new tariffs are reshaping the US's share in global mining, we first analyze from the perspective of returns.

The following graph shows the estimated payback period for deploying an Antminer S21+ in the US and a country unaffected by tariffs. As the data shows, overpaying by 24% for the same mining machine in the US significantly extends the payback period—undermining the core economic rationale for mining in the US.

In addition to the higher mining machine cost, the risk aspect has also been impacted. Many US miners felt reassured during the Trump administration, expecting a stable regulatory environment. But they are now experiencing the flip side of his policy volatility. Even if these tariffs are rescinded within months, the damage has been done—the confidence in long-term planning has been shaken. In a scenario where key variables could change overnight, few are willing to make significant investments.

In any case, the once unparalleled risk-return balance of U.S. Bitcoin mining has significantly deteriorated. This change could lead to a gradual decline in the U.S.' share of the global mining industry relative to other countries.

Of course, existing mining machines already imported into the U.S. will not be affected—miners have no reason to shut them down. However, the path to expansion has now become steep and filled with uncertainty.

Meanwhile, miners in tax-free jurisdictions will continue to scale up, solidifying their competitive advantage. Therefore, it is expected that the U.S.' global hash rate share will decrease—not because miners are exiting, but because they are no longer growing.

From a broader perspective, this could lead to a more diverse geographical distribution of Bitcoin mining than ever before. While the U.S. will still be a major player, its dominance will weaken, and the global hash rate distribution will become more balanced. This aligns with predictions from Braiins' Kristian Csepcar and Bitmars' Summer Meng.

Network Hash Rate Growth Will Slow Down

In the previous section, we explained how the new tariffs could lead to a decrease in the U.S.' share of the global Bitcoin mining industry. Given the U.S.' significant role in global hash rate, its slowdown—or even halt—in growth will inevitably result in an overall deceleration of global hash rate growth.

According to Hashrate Index data, as of the second quarter of 2025, the U.S. accounts for approximately 36% of the global hash rate. In contrast, CBECI data shows that as of January 2022, the U.S.' hash rate share was around 38%. This suggests that over the past three years, the growth rate of the U.S. mining industry has been roughly in line with other regions worldwide.

If this growth trajectory were to continue, the U.S. would contribute around 36% to future global hash rate growth. Therefore, if the U.S. mining industry stagnates due to tariffs' impact, it could lead to a reduction in the global hash rate growth rate of up to 36%.

However, the likelihood of a complete halt in U.S. mining industry growth is very low. As we will explain in the next section, these tariffs may be temporary, and there may be ways to circumvent them in the future. Therefore, the more realistic expectation is that the U.S. mining industry will continue to expand, but at a much slower pace than before. The assumption of a 36% reduction in global hash rate growth should be seen as an absolute upper limit—the actual impact may be slightly lower.

In the long run, if U.S. growth slows down or stalls, miners from other countries may accelerate their expansion to gradually fill this gap.

Nevertheless, in the short to medium term—within the next year or two—we may see global hash rate growth slower than previously expected. In an industry where slower hash rate growth translates to higher earnings, this will be a welcome development for miners worldwide.

Is This Temporary or Permanent?

So far, this article has taken a rather pessimistic view of how these tariffs could impact the U.S. Bitcoin mining industry—an outlook that is understandable given the immediate and severe effects they could bring about. However, the situation is more nuanced, and there are some crucial questions worth exploring.

In the following sections, we will address these questions and assess how the long-term prospects of the U.S. mining industry could cope with the current challenges.

Will Trump repeal the tariffs after implementing them for a few months?

It is entirely possible—especially considering the unpredictable and reactive nature of Trump's policy-making style. If the tariffs are repealed, U.S. miners would once again be able to import mining equipment at competitive prices, alleviating many of the immediate pressures they face.

However, the damage to long-term investor confidence may already have been done. Even if the tariffs are lifted, the sudden introduction of them has made large-scale, long-term investments in the U.S. mining industry more challenging. In a capital-intensive industry like Bitcoin mining, policy stability is crucial—and right now, that is in short supply.

Can mining equipment manufacturers circumvent the tariffs by importing chips from China Taiwan and assembling the miners in the U.S.?

Mining equipment manufacturers may indeed circumvent the tariffs by importing chips from China Taiwan and assembling miners locally in the U.S. According to the White House's official statement, semiconductors are not subject to the reciprocal tariffs. This means that chips can be imported into the U.S. duty-free. However, local production of miners in the U.S. still requires other components, many of which have become more expensive due to tariffs, leading to overall economic inflation in the U.S.

Currently, manufacturers like MicroBT have established assembly lines in the U.S., but Bitmain has yet to follow suit. Even with MicroBT's assembly capabilities, their production capacity is far from sufficient to meet U.S. demand for miners in the next 1-2 years.

Therefore, while this option is technically viable, it does not address the immediate concerns of U.S. miners. However, in the long run, we anticipate more miner assembly gradually shifting to the U.S. as manufacturers adapt to the new tariff environment and expand local production capacity. This transition may help reduce reliance on international imports and lessen the impact of tariffs over time.

Is it realistic to establish a complete Bitcoin mining hardware supply chain in the United States from chip manufacturing to final assembly?

Establishing a full Bitcoin mining hardware supply chain in the United States from chip manufacturing to final assembly is a complex challenge, despite strong advocacy from the Bitcoin mining industry and political leaders for localized chip production. Currently, the most advanced chips used in Bitcoin mining are manufactured in Taiwan and South Korea, regions with decades of expertise and finely tuned supply chains. The United States' reliance on key components from Asian countries poses a significant geopolitical risk not only to the Bitcoin mining industry but to the entire high-tech sector.

While localizing mining rig assembly in the U.S. is feasible, continued dependency on imported chips remains a major hurdle. Companies like Bitmain, MicroBT, and Canaan could establish assembly lines in the U.S., with new players such as Auradine also eyeing this market. However, without domestically produced cutting-edge chips, these manufacturers will still rely on imports in the foreseeable future.

Kristian Csepcsar from Braiins further emphasized this challenge, saying: "Chip foundries have started setting up manufacturing facilities in the U.S., but they are starting from a high nanometer level. It takes years to nurture talent and expertise to transition to lower nanometer levels. This is a progressive process—companies start with high nanometer chips to ensure a return on investment, then strive to expand to more advanced technology. Even as the U.S. progresses, establishing a fully localized Bitcoin mining hardware supply chain is nearly impossible due to the high costs. The real question is, if demand is high, whether it is still cheaper to manufacture in China and pay tariffs. After all, starting end-to-end manufacturing in the U.S. requires time and substantial investment, just as Bitmain recently attempted to set up assembly lines in China—although there has been little news since."

In summary, while the U.S. has great potential in assembly and chip manufacturing, a fully localized Bitcoin mining hardware supply chain remains a long-term goal rather than a short-term reality. The cost, time, and complexity of this transition make it unlikely to be achieved on a large scale in the coming years.

Conclusion

In conclusion, the newly implemented import tariffs will significantly impact the U.S. Bitcoin mining industry—leading to price increases for hardware, a decrease in U.S. market share, and a slowdown in global hash rate growth—but the long-term implications are more intricate.

As events unfold, miners and industry stakeholders need to closely monitor the political and economic landscape to address potential tariff and policy changes. The U.S. mining industry may face challenges in the short term, but there are still opportunities for growth and adaptation within the global mining ecosystem.

You may also like

Bitcoin ETF Outflows Hit a Record $4.4 Billion: What Are Traders Doing With Their Cash?

WEEX App Just Got Smarter – New Tabs for Faster Trades & Easy Asset Management

Blockchain Capital Partner: The Core Secret of Arbitrage

WEEX All-New Search Features: Find, Trade & Earn Faster Than Ever

Will MicroStrategy fall into a death spiral? What will the macro trend be in the second half of the year?

Morning Report | Illinois signs the strictest digital asset tax law in the U.S.; RWA tokenization market size surpasses $43 billion, institutions accelerate the migration of on-chain assets

Full version of the debut Q&A! Federal Reserve Chairman Waller: Sticking to the 2% inflation target, establishing five special working groups, individual did not submit the dot plot

From Disruptor to Shadow Market: The Crypto Market is Becoming a Colony of Traditional Finance

Dalio's important long article: How to position in the current market environment?

OKX Star analyzes Binance's competitive advantages: when regulation levels the playing field, competition has just begun

New gameplay for participating in initial offerings on cryptocurrency exchanges

Why Is Bitcoin Down Today? What the Hawkish FOMC Means for SpaceX, Gold and Nasdaq

DeepSeek Financing Story

Morning Report | DeepSeek completes over $7 billion in financing, with a valuation exceeding $50 billion; Musk's personal wealth has surpassed the total market value of Bitcoin

Cursor, why did you get on Musk's spaceship?

In the name of charity, for the benefit of the family: How the Trump family turned charity into profit?

Will Gold Break $4,500 After Tonight's Fed Decision? What XAUT and PAXG Traders Need to Know